Navigating AARP Plan F Premiums: A Comprehensive Guide

Healthcare costs can feel like a maze, especially as we age. For many, supplemental insurance, often called Medigap, offers a way to navigate these complexities. AARP Plan F, once a popular choice, presents a specific set of premium considerations. This comprehensive guide aims to demystify AARP Plan F premium pricing, exploring the factors influencing its cost and providing insights for informed decision-making.

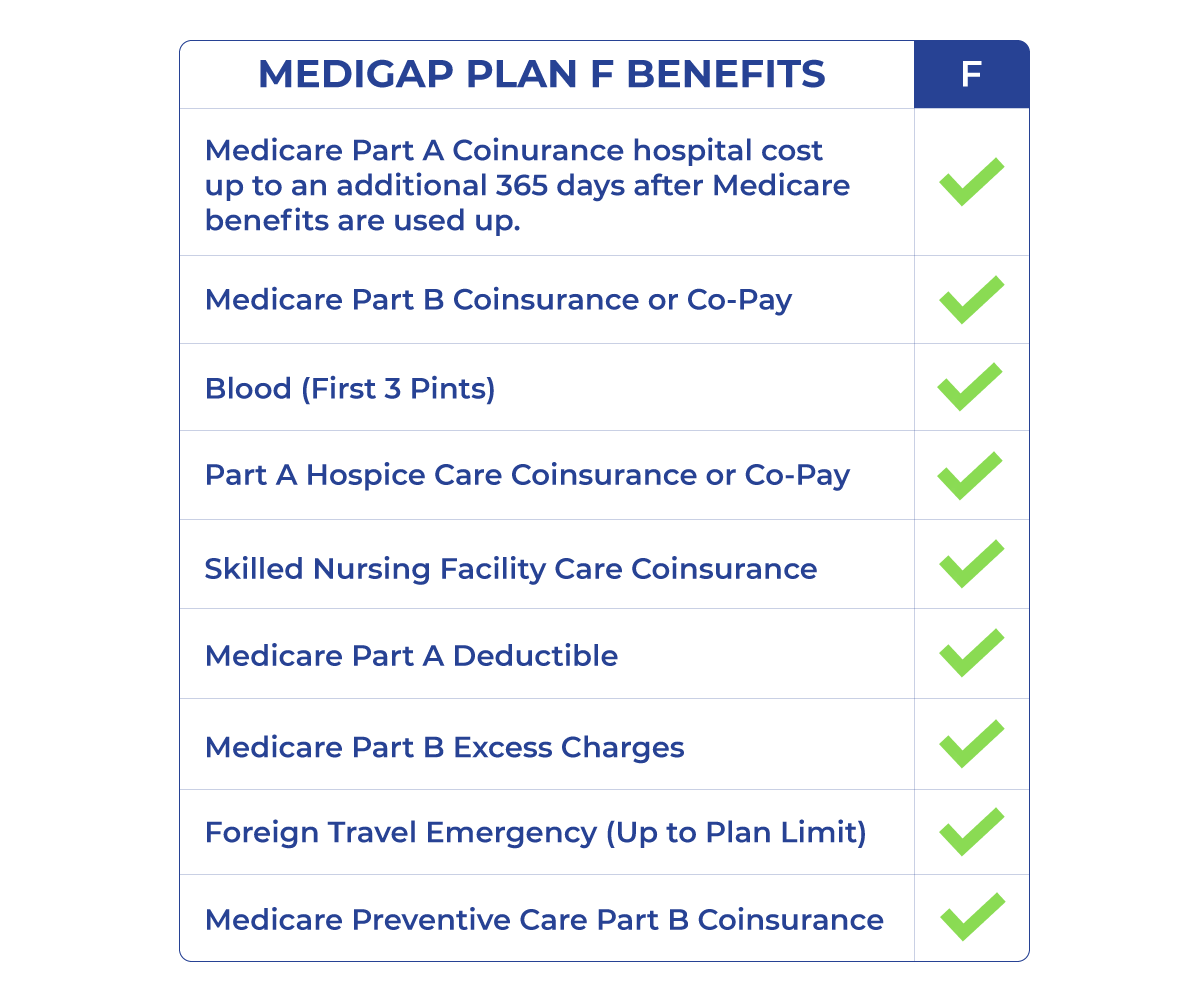

Understanding the landscape of AARP Plan F premiums requires a grasp of the policy itself. Plan F was designed to cover the "gaps" in Original Medicare (Parts A and B), offering comprehensive protection against out-of-pocket expenses like copayments, coinsurance, and deductibles. However, changes in Medicare legislation have impacted the availability of Plan F for new beneficiaries.

The history of AARP Plan F premiums is intertwined with the evolution of Medigap. As healthcare costs rose, the need for supplemental coverage grew, leading to the development of standardized Medigap plans, including Plan F. AARP, a prominent organization advocating for seniors, partnered with insurers to offer these plans, including Plan F, to its members. This arrangement provided access to Medigap coverage, often with competitive premiums due to AARP's large membership base.

AARP Plan F premiums are determined by several factors. These can include age, location, tobacco use, and the chosen insurance company. The pricing structure itself can vary. Some insurers use “attained-age” rating, meaning premiums increase as you get older. Others use “issue-age” or “community-rated” pricing, where the premium is based on your age when you first enroll and generally increases less dramatically over time.

One of the key considerations with AARP Plan F is its current availability. For individuals newly eligible for Medicare after January 1, 2020, Plan F is no longer an option. This change, brought about by the Medicare Access and CHIP Reauthorization Act (MACRA), aimed to encourage cost-consciousness among beneficiaries. However, those who were already enrolled in Plan F before this date can continue their coverage.

Existing Plan F beneficiaries should carefully consider their current premiums and compare them with other Medigap options. Plans G and N, for example, offer similar coverage with slightly different cost-sharing structures. Evaluating these alternatives could potentially lead to premium savings.

While AARP does not directly set Plan F premiums, they endorse plans offered by UnitedHealthcare Insurance Company. Therefore, understanding UnitedHealthcare's pricing methodologies and available discounts is essential for AARP members considering or already enrolled in Plan F.

Navigating the complexities of Medicare supplemental insurance requires diligent research. Resources such as the Medicare.gov website and AARP's own publications can provide valuable insights into plan options and associated costs.

Advantages and Disadvantages of AARP Plan F

| Advantages | Disadvantages |

|---|---|

| Comprehensive coverage, predictable out-of-pocket costs | No longer available to new Medicare beneficiaries |

| Potentially simplifies medical budgeting | Can be more expensive than other Medigap plans |

Frequently Asked Questions

1. What is AARP Plan F? AARP Plan F is a Medicare Supplement Insurance plan offered through UnitedHealthcare that helps cover out-of-pocket costs associated with Original Medicare.

2. Who is eligible for AARP Plan F? Generally, only individuals who were eligible for Medicare before January 1, 2020, can enroll in Plan F.

3. How much do AARP Plan F premiums cost? Premiums vary based on factors such as age, location, and the insurer.

4. Can I switch from AARP Plan F to another Medigap plan? Yes, you can switch Medigap plans, but you may undergo medical underwriting.

5. Does AARP Plan F cover all medical expenses? Plan F covers most out-of-pocket costs associated with Original Medicare, but not everything, such as Part B excess charges.

6. Where can I find more information on AARP Plan F premiums? The Medicare.gov website and AARP's resources provide details on Medigap plans.

7. How do I find the best AARP Plan F premiums in my area? Comparing quotes from different insurers is essential for finding the best rates.

8. What is the difference between AARP Plan F and Plan G? Plan G is a similar option but requires beneficiaries to pay the Part B deductible.

Tips and tricks for managing AARP Plan F premiums include comparing rates annually, considering household discounts if available, and understanding your specific healthcare needs to ensure you have the right coverage level.

In conclusion, understanding AARP Plan F premiums is crucial for both current and prospective beneficiaries. While Plan F is no longer accessible to new Medicare enrollees, existing members should evaluate their options, considering the plan's comprehensive coverage and potential cost implications. Comparing rates, understanding the various factors impacting premiums, and staying informed about changes in Medicare regulations are essential steps in navigating the landscape of supplemental insurance and making informed decisions about your healthcare needs. Take the time to research your options, compare quotes, and choose a plan that aligns with your budget and coverage requirements. Reaching out to a licensed insurance broker specializing in Medicare can also provide personalized guidance and help clarify complex details, enabling you to navigate the Medicare landscape with confidence.

Unveiling hidden truths shared between siblings

Decoding the virginia beach gs pay scale mystery

Shimmer and shine behr premium plus pearlescent paint deep dive

{kind=link}